SBI Cashback Credit Card Review: The Don Cashback Card which can save upto 30%

The Indian credit card market has become crowded with complicated reward structures. Some cards work best on travel portals, some only make sense if you transfer points to airlines, some are useful only inside one app ecosystem, and some look attractive until you start reading the exclusions.

In the middle of all this, the SBI Cashback Credit Card continues to remain one of the simplest cards to understand that helps users to save upto 30% on their purchase.

It is not a premium card. It is not a travel card. It is not a lounge card. It is not a card that will help you unlock business class seats or hotel upgrades.

It is a cashback card built mainly for online spends. And for the right user, that is exactly what makes it valuable.

What SBI Cashback Credit Card Offers

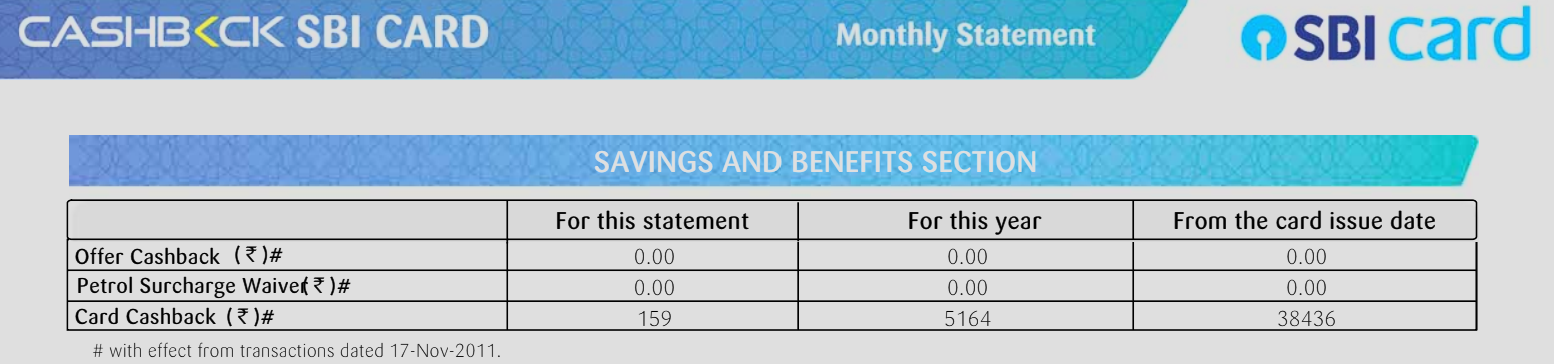

The SBI Cashback Credit Card gives 5% cashback on eligible online spends and 1% cashback on eligible offline spends.

The online cashback is capped at ₹2,000 per statement cycle. The offline cashback is also capped at ₹2,000 per statement cycle. The total cashback across online and offline spends cannot exceed ₹4,000 in one statement cycle.

This means the most important number for this card is ₹40,000.

If you spend around ₹40,000 on eligible online transactions in a statement cycle, you can earn ₹2,000 cashback. After that, the online cashback cap is exhausted for that cycle.

This is the cleanest way to look at the card.

It is not a card where you should keep pushing every spend blindly. It is a card where you should use it till the point where it gives maximum value, and then move the remaining spends to another card.

For a regular online shopper, ₹40,000 is a very practical monthly limit. It can include shopping, groceries, fashion, food delivery, electronics, subscriptions and other eligible online spends. And read till the date you will learn how to save upto 30% without breaching Rs 40,000 limits.

That is why the card still has a strong place in many wallets despite the devaluation.

Where The Card Works Best

The SBI Cashback Credit Card works best for normal online spends.

This includes eligible spends on shopping platforms, food delivery apps, grocery apps, fashion websites, subscriptions, electronics, personal care and other online merchants.

The biggest advantage is that the card is not locked to one merchant. You are not forced to spend only on one specific app to get value just like ICICI Amazon Pay credit card or Axis Flipkart Credit Card.

That makes it very useful for people whose online spending is spread across multiple platforms.

A lot of cashback cards look better on paper because they offer a higher percentage on selected brands. But the moment your spends move outside that ecosystem, the value drops. SBI Cashback is more flexible because it is designed around eligible online spends as a broader category.

This is the main reason the card has survived so many market changes. It is simple, broad and practical.

The Real upto 30% savings blueprint: Voucher Stacking With SBI Cashback

Most people look at the SBI Cashback Credit Card as a simple 5% online cashback card. That is correct, but it is not the full story.

The real value of this card starts showing when you combine its 5% online cashback with discounted brand vouchers available on platforms like Amazon. This is where the effective savings can move meaningfully beyond the standard 5%.

Depending on the voucher discount, your total savings can move to 10%, 15%, 20% or even higher. In some cases, where the brand voucher itself is available at a deep discount and the transaction remains eligible for SBI Cashback, the combined savings can move towards the 5% to 30% range.

This is why SBI Cashback continues to remain one of the most interesting online-spend cards for optimizer. The card is not powerful only because it gives 5% cashback. It becomes powerful because that 5% can be stacked smartly on top of existing voucher discounts.

How The Voucher Route Works

SBI Cashback does not give cashback on excluded categories, and gift cards can be tricky because cashback eligibility depends on how the transaction is processed.

However, when you buy certain brand vouchers from Amazon, the transaction may not always get processed under a gift card MCC. In many cases, it may appear under an Amazon shopping-style merchant descriptor or an eligible shopping category.

If the transaction is processed under an eligible MCC, SBI Cashback may give the regular 5% online cashback on that purchase.

This creates two layers of savings. The first layer is the instant discount available on the voucher. The second layer is the 5% cashback from SBI Cashback, provided the transaction remains eligible.

This is where the card becomes far more interesting than a basic 5% cashback product. Few examples of brand vouchers listed below. You can get extra 5% cashback over and above discount available.

| # | Brand | Common Use Case | Instant Discount Visible |

|---|---|---|---|

| 1 | Amazon Pay | Everyday payments | No instant discount visible |

| 2 | Amazon Shopping | Shopping | No instant discount visible |

| 3 | BigBasket | Groceries | 3% off |

| 4 | Blinkit | Quick commerce | 2% off |

| 5 | Zepto | Quick commerce | No instant discount visible |

| 6 | Uber | Cabs / travel | 4% off |

| 7 | Domino’s Pizza | Food delivery / dining | 14% off |

| 8 | KFC | Food / QSR | 4% off |

| 9 | PVR INOX Cinemas | Movies | 20% off / 19% off |

| 10 | BookMyShow | Movies / events | 2% off |

| 11 | Myntra | Fashion | 2% off |

| 12 | AJIO | Fashion | 4% off |

| 13 | Nykaa | Beauty | 4% off |

| 14 | Apollo Pharmacy | Pharmacy / health | 8% off / 6% off |

| 15 | MakeMyTrip | Travel | 6% off |

| 16 | Goibibo | Travel | 5% off |

| 17 | Croma | Electronics | No instant discount visible |

| 18 | Reliance Smart Super Store | Grocery / retail | 2% off |

| 19 | Starbucks | Coffee / cafes | 6% off / 5% off |

| 20 | Lenskart | Eyewear | 10% off / 9% off |

| # | Voucher | Instant Discount Visible |

|---|---|---|

| 1 | PVR INOX Cinemas | 20% off / 19% off |

| 2 | Zee5 | 19% off |

| 3 | Naturals Salons | 17% off |

| 4 | Mainland China | 20% off |

| 5 | Lionsgate Play | 20% off |

A Simple Example

Suppose a Baskin Robbins voucher is available on Amazon at 12% instant discount.

You buy that voucher using your SBI Cashback Credit Card. If the transaction is processed under an eligible MCC and cashback is posted, your total savings become approximately 17%.

That includes the 12% instant discount on the voucher and 5% cashback from SBI Cashback.

The same logic applies to other brand vouchers as well. If a Coach voucher is available at 10% discount and SBI Cashback posts 5% cashback, your effective savings can move to around 15%. If a DailyObjects voucher is available at 9% discount and the 5% cashback is posted, your total savings can move to around 14%.

For food, fashion, travel, health, lifestyle and D2C brand vouchers, the final savings will depend on the live voucher discount and whether the transaction remains eligible for cashback.

This is how a simple cashback card starts behaving like a proper optimization tool.

The Amazon Pay Voucher Game for Utility Bills

Many credit card optimizers use SBI Cashback for buying eligible Amazon Pay vouchers online and then use the balance for payments where direct cashback may not be available.

This can sometimes be useful for categories like recharges or utility payments, depending on the voucher type, merchant treatment and latest bank rules.

But this should not be treated as a permanent guaranteed hack.

Banks can change terms. Merchants can change MCCs. Voucher eligibility can change. Cashback behavior can also vary.

The smarter approach is to test with a small transaction first. Once cashback is posted, then decide whether it is worth scaling.

Never build a large monthly strategy on assumption.

Where This Strategy Can Be Useful

The voucher route can be useful across multiple categories, depending on live voucher availability and discounts.

You may find useful vouchers across brands like Baskin Robbins, Blinkit, Coach, DailyObjects, Frido, Lifestyle, Diesel, Domino’s, EaseMyTrip, Goibibo, HealthKart and many more.

The key is to buy vouchers only for brands where you were already planning to spend. If you were anyway going to order food, book travel, buy apparel, shop for accessories, purchase fitness products or spend on a lifestyle brand, buying a discounted voucher first can improve your effective return.

But buying vouchers only because they are discounted is not optimization. It simply locks your money into future spending.

Smart optimization reduces the cost of planned spends. It should not create unnecessary spends.

The OTP Keyword Check

Before completing a voucher transaction on Amazon, always check the OTP message carefully.

If the OTP message clearly shows wording like “Amazon Gift Card”, it may indicate that the transaction is being processed as a gift card-type transaction. If your goal is to earn SBI Cashback, it is safer to avoid proceeding with that transaction.

On the other hand, if the OTP message shows descriptors like ASSPL, Amazon Pay, Amazon Retail or a normal Amazon shopping-style descriptor, the transaction may have a better chance of falling under an eligible online shopping category.

This is not a guarantee of cashback, but it is a useful first-level check before completing the payment.

For serious optimization, this small step matters.

MCC Verification Is Non-Negotiable

The biggest mistake users make with voucher stacking is assuming that every voucher transaction will behave the same way.

It will not.

MCCs can change. Merchant descriptors can change. Amazon can route different voucher purchases differently. Bank treatment can change. SBI can also update its cashback logic at any point.

So before making a large voucher purchase, always test with a small transaction.

Buy a small-value voucher first. Check the OTP descriptor. Let the transaction settle. Track whether cashback gets posted after statement generation. Only after this should you scale the amount.

This one habit can save you from unnecessary disappointment.

The Book1A rule is simple: test first, track properly, and scale only after confirmation.

Why This Makes SBI Cashback Powerful

This is the reason SBI Cashback continues to remain one of the most useful cards for online spend optimization.

On paper, it is a 5% online cashback card. But when used with discounted vouchers, it can deliver much stronger effective savings on planned spends.

Food, fashion, grocery, travel, electronics, health, lifestyle and D2C purchases can become far more rewarding if the right voucher is available and cashback eligibility is confirmed.

This is where SBI Cashback moves from a beginner-friendly cashback card to an advanced optimization card.

A normal user sees 5%.

An optimizer sees 5% cashback, voucher discount, planned spending and MCC discipline working together.

That is the difference.

Important Caution

This route should be used responsibly.

Do not assume every Amazon voucher purchase will earn cashback. Do not make large transactions without testing. Do not buy vouchers for brands you may not use. Do not use this route for business spends. Do not treat any MCC behavior as permanent.

The bank’s terms, merchant category codes and transaction descriptors always matter.

Voucher stacking is powerful only when done with discipline.

Used casually, it can create confusion. Used properly, it can turn SBI Cashback into one of the sharpest online savings cards in India.

Where The Card Does Not Work

This is where users need to be careful.

SBI Cashback does not give cashback on several important categories. These include fuel, rent, wallet loads, school and educational services, insurance, utilities, railways, jewellery, tolls, government transactions, gift card and novelty shops, quasi-cash or financial institution transactions and digital gaming platforms.

So, this is not a card for every payment.

If you pay electricity bills directly using this card, you should not expect cashback. If you pay insurance premium directly, it is not the right card. If you use it for rent, education, fuel or wallet loading, the cashback story does not work.

This is the most common mistake people make with cashback cards.

They see the headline number and assume it applies everywhere.

It does not.

The SBI Cashback Credit Card is powerful only when it is used in the correct category.

The Real Sweet Spot: ₹40,000 Online Spends

The ideal monthly usage for this card is simple.

Use it for eligible online spends up to around ₹40,000 per statement cycle.

At 5%, this gives you ₹2,000 cashback, which is the online cap.

After that, additional online spends in the same statement cycle will not earn more online cashback. So it makes sense to shift the remaining spends to another card.

This is how a good credit card setup should work.

SBI Cashback should be your online spending card. A RuPay credit card can handle UPI spends. A fuel card can handle fuel. A travel card can handle flights, hotels, lounges and forex. A premium rewards card can handle spends where points or miles give better value.

The card is excellent when you give it one job.

The problem starts when you expect one card to do everything.

Cashback Redemption Is Simple

One of the best parts of this card is the redemption process.

There is no redemption process.

The cashback is automatically credited to your SBI Card account after statement generation. You do not need to redeem reward points, select vouchers, pay redemption charges or track expiry dates.

This makes the card very beginner-friendly.

A lot of users lose value in reward-point cards because they either redeem poorly or do not redeem at all. SBI Cashback avoids that entire problem.

The cashback directly reduces your card outstanding.

That said, the statement does not show a clean transaction-wise cashback breakup. So if you want to audit every transaction, you may need to calculate it manually.

For casual users, this is not a major issue. For serious optimizers, it is slightly annoying but manageable.

Cashback On Returns And Cancellations

Cashback is not final if the transaction itself is reversed.

If you cancel an order, return a product or receive a refund, the cashback linked to that transaction can also be reversed and adjusted in a later statement.

This is normal, but important to remember.

Do not count cashback as final until the transaction is fully settled and you are sure there is no return or cancellation involved.

No Lounge Access, And That Is Fine

The SBI Cashback Credit Card does not offer domestic or international airport lounge access.

For some users, this may look like a drawback. But this card should not be judged like a travel card.

It is not meant for lounges. It is meant for online cashback.

If lounge access matters to you, pair this card with a separate travel or premium card. That is a better approach than expecting SBI Cashback to do everything.

A good card wallet is not about finding one perfect card. It is about assigning the right role to each card.

SBI Cashback’s role is clear: eligible online spends.

Fuel Surcharge Waiver

The card does not offer cashback on fuel transactions.

However, it does offer a 1% fuel surcharge waiver on fuel transactions between ₹500 and ₹3,000 at petrol pumps across India. The waiver is capped at ₹100 per statement cycle.

This is a small benefit, not the main reason to get the card.

If your monthly fuel spends are high, you should look at a proper fuel card instead. Cards like SBI BPCL Octane or other fuel-focused cards will usually make more sense for that category.

Forex Markup And International Usage

This is not a good card for international spends.

The card carries a foreign currency markup of 3.5% plus GST. That makes it weak for foreign currency transactions.

Even if an international transaction is online, the forex markup can destroy the cashback value. For foreign spends, a zero-forex or low-forex card will be much better.

So the positioning is very clear.

Use SBI Cashback for domestic eligible online spends. Do not make it your default card for international transactions.

Cash Withdrawal And Interest Charges

This card should not be used for cash withdrawals.

The cash advance charges are high, and interest costs can become painful very quickly if you do not pay the full bill on time.

This is true for most credit cards, but it is especially important for cashback users to remember. Earning 5% cashback makes no sense if you are paying interest on your outstanding balance.

The rule is simple.

Use the card. Earn cashback. Pay the full bill before the due date.

The moment you start revolving credit, the reward game is over.

Online Sale Discount Limitation

One practical drawback of the SBI Cashback Credit Card is that it may not always be eligible for SBI bank instant discount offers during major online sales.

This creates confusion because many people assume every SBI Card should work during SBI sale offers.

That is not always the case.

During Amazon, Flipkart or other sale events, SBI Cashback may be excluded from instant bank discounts depending on the offer terms.

So, during sale periods, compare both options.

If another SBI credit card is giving 10% instant discount, and SBI Cashback gives only 5% cashback later, the instant discount card may be better for that transaction.

This is where optimization matters.

Do not stay loyal to one card. Stay loyal to the best return.

Fees And Annual Waiver

The card comes with a joining fee of ₹999 plus GST and an annual renewal fee of ₹999 plus GST.

The annual fee can be waived if you spend ₹2 lakh or more in the previous membership year.

For someone who shops online regularly, the fee is not difficult to justify. Even ₹20,000 of eligible online spends can generate around ₹1,000 cashback. So the annual fee can be recovered fairly quickly if the card is used properly.

But this card should not be picked just because everyone calls it a good cashback card. It should be picked only if your actual spending pattern supports it. If most of your monthly spends are offline, rent, insurance, fuel, education fees, utilities or business payments, this card may not deliver the value you expect.

Pro Tip: Once your annual fee is charged. You can call SBI customer care and request for fee waiver. Basis on your relationship. SBI may waive off fees. Many community members managed to waive off the annual fee.

By the way, this is exactly why we are building Book1A.

Most people have credit cards, reward points, vouchers, miles, hotel memberships and offers scattered across different apps, emails, screenshots and memory. The problem is not just earning points. The real problem is knowing what you own, where it can be used, when it expires, and how to extract the best value from it.

That is where Book1A starts.

Our free Onboarding plan gives you access to your own Book1A dashboard, where you can track your cards, points, miles, vouchers, expiry dates, transfer routes, hotel deals, Store1A offers and important rewards updates in one place. It is built for anyone who wants their points life to finally feel organised.

But if you want to go beyond tracking and actually build a strategy, Book1A also offers personalised credit card consultancy.

Because your points were never meant to sit idle. They were meant to take you somewhere.

We help you build a personalised roadmap for your cards, spends, points, miles and travel goals. From choosing the right card for the right expense to optimising reward points, milestone benefits, transfer partners, hotel stays and flight redemptions, we create a clear strategy around your lifestyle.

This is for people who want to enjoy the real power of credit card rewards without spending hours doing maths, comparing permutations, checking caps, reading fine print and second-guessing every redemption.

You focus on better vacations, better hotels, better flights and better savings.

We focus on the strategy.

A free dashboard to bring everything in one place.

A paid consultancy layer when you want a complete credit card and rewards roadmap.

And a smarter way to make your points work harder for you.

Who Should Get This Card

You should consider SBI Cashback if your monthly online spends are regular and meaningful.

If you shop across multiple online platforms, order groceries online, use food delivery apps, buy fashion and electronics online, pay for subscriptions and prefer direct cashback over reward points, this card makes a lot of sense.

It is also a good card for beginners because there is no complicated redemption system.

You do not need to understand airline miles. You do not need to learn hotel transfer partners. You do not need to search award seats. You just need to use the card in the right category and pay the bill on time.

For many users, that simplicity is valuable.

Who Should Avoid This Card

Avoid this card if most of your spends are in excluded categories.

If your biggest monthly spends are insurance, rent, education fees, fuel, utility bills, wallet loading or government payments, this card will not help much directly.

Also avoid using it as a travel card. It has no lounge access and carries a high forex markup.

If you are already using premium credit cards and can consistently extract higher value through points, miles or hotel transfers, SBI Cashback may not be your primary card. But even in that case, it can still work as a simple online cashback card.

Final Verdict

The SBI Cashback Credit Card is not exciting in a premium-card way.

It does not give airport lounges, hotel benefits, luxury privileges or travel status. But it gives something that is equally useful for a large number of users: straightforward cashback on eligible online spends.

That is why the card still remains relevant.

For someone who spends regularly online, SBI Cashback can be one of the most practical cards to keep. The key is to use it with discipline.

Use it for eligible online spends. Respect the ₹2,000 online cashback cap. Avoid excluded categories. Do not use it for forex. Do not expect it to work for every instant discount offer. And do not use it blindly after the cap is exhausted.

This is not a card that tries to do everything.

It is a specialist card.

And when used in the right place, it is still one of the cleanest cashback machines in India.

Featured card

Cashback SBI Card

₹999 join · 5% cashback on online spends

Complimentary Runway Plan when your new card is activated

Apply now