Axis Atlas EDGE Miles Can Now Pay Your Credit Card Bill: The Card Just Became More Flexible

Axis Bank has made a very interesting update for Axis Atlas credit cardholders. You can now use the EDGE Miles earned on your Axis Atlas Credit Card to pay your credit card bill, at a value of 1 EDGE Mile = ₹1.

This is a major shift in how Atlas should be understood. Until now, the strongest use case of Axis Atlas was clear: earn EDGE Miles, transfer them to airline or hotel partners, and extract value through award flights or hotel stays. With this new option, Atlas no longer remains only a miles-first travel card. It now gets a fixed-value redemption route as well.

In simple terms, Axis Atlas now offers the best of both worlds. It can act like a miles card when you want to chase travel value, and it can act like a cashback-style card when you want simple, predictable value against your credit card bill.

What has changed?

The new redemption option allows Axis Atlas cardholders to burn EDGE Miles towards credit card bill payment at a clean fixed value:

1 EDGE Mile = ₹1

So if you have 6,000 EDGE Miles, you can use them to get ₹6,000 value against your credit card bill.

This is simple, direct and easy to understand. There is no award availability, no loyalty program confusion, no transfer delay and no need to calculate hotel or flight redemption value. You earn EDGE Miles and use them like a cash-style credit against your bill.

But this is only one side of the story.

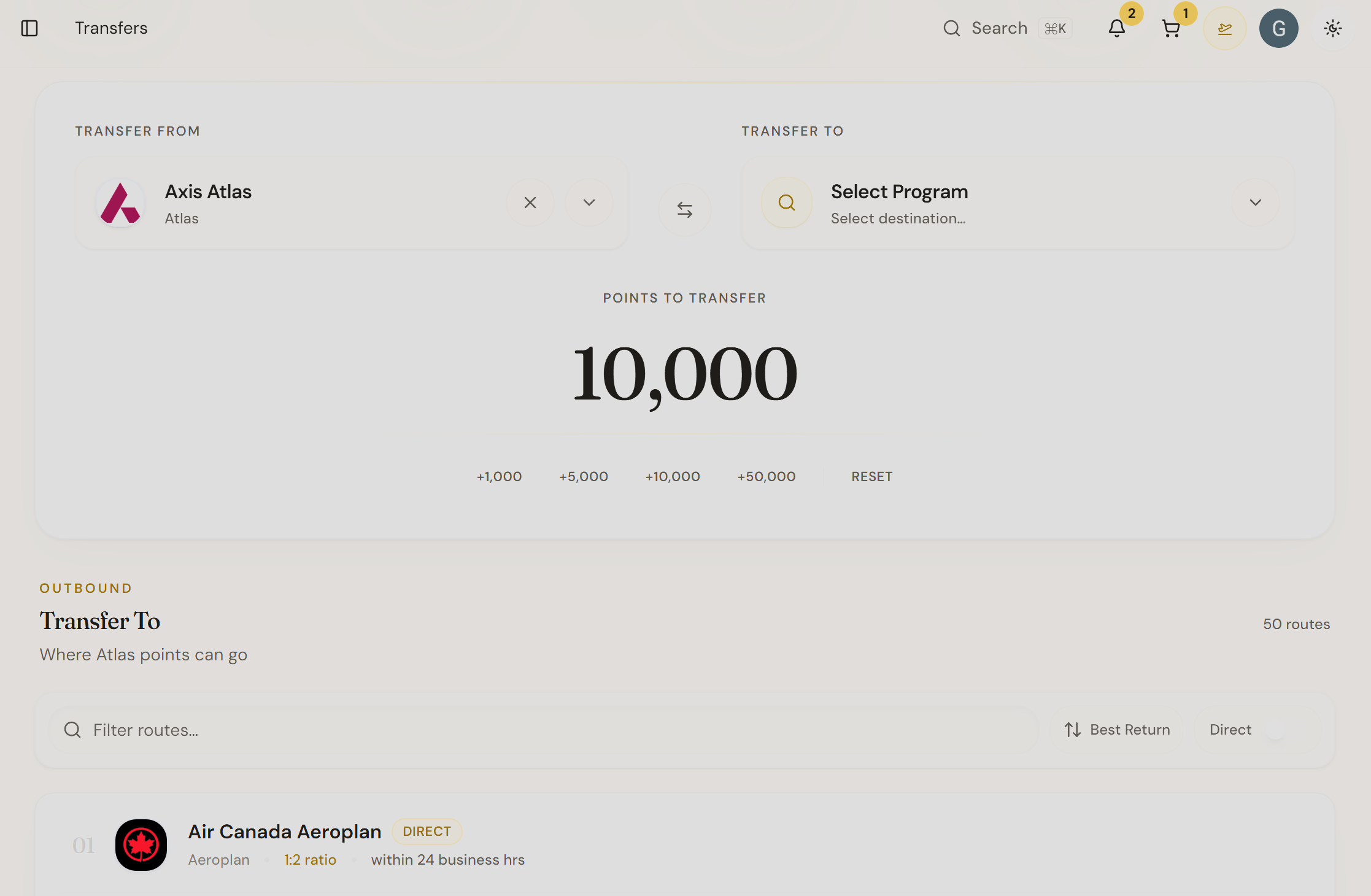

The bigger strength of Axis Atlas has always been the transfer partner route. When you transfer EDGE Miles from Axis Atlas to airline or hotel partners, the usual ratio is:

1 EDGE Mile = 2 partner miles or hotel points

For example, if you transfer 6,000 Axis Atlas EDGE Miles to Air India Maharaja Club, you get 12,000 Maharaja Points. Similarly, if you transfer 6,000 EDGE Miles to ITC, you get 12,000 ITC points.

This is where the decision becomes interesting. The same 6,000 EDGE Miles can either give you ₹6,000 value against your credit card bill, or they can become 12,000 airline or hotel points through transfer partners.

You can check all the transfer partners for Axis Bank for Free at Book1A Dashboard.

Fixed value vs travel value

The new bill payment option gives Axis Atlas users a guaranteed value floor. You now know that every EDGE Mile can be worth ₹1 if you want to keep things simple.

But transfer partners can still offer better value if used properly. The 1:2 transfer ratio is powerful because your EDGE Miles double when moved to partner programs. That creates a chance to unlock higher value through award flights and hotel stays.

Let’s take a simple example.

If you have 6,000 EDGE Miles, you can redeem them for ₹6,000 credit card bill payment value. That is straightforward.

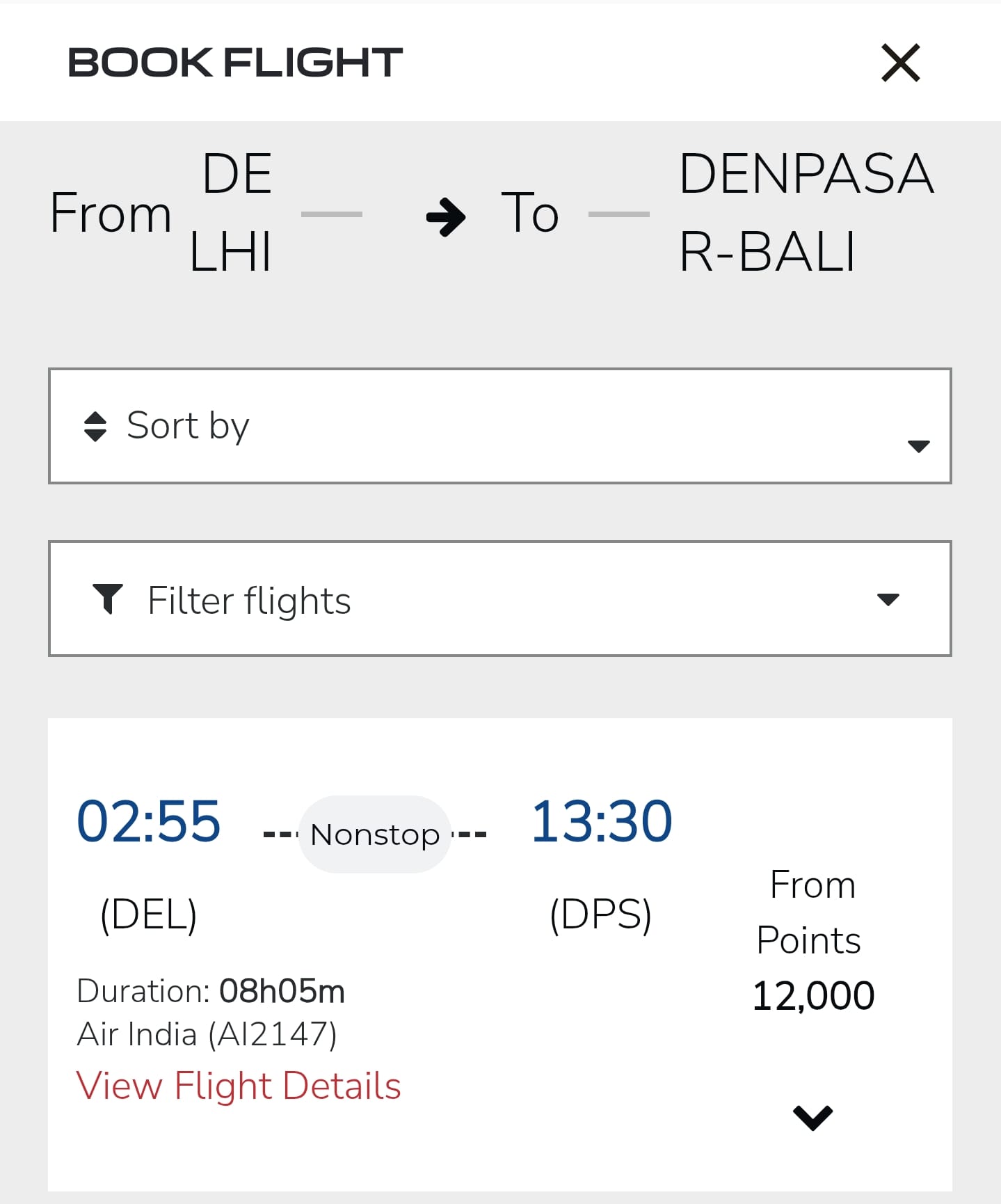

But if you transfer the same 6,000 EDGE Miles to Air India, you get 12,000 Maharaja Points. If an award seat is available, those 12,000 points may help you book a flight like Delhi to Bali with taxes and charges extra. In that situation, the value you extract from the transfer route can be much higher than ₹6,000.

This does not mean transfer partners will always win. It means transfer partners have upside. Bill payment gives certainty. Travel redemption give potential.

Why this update makes Axis Atlas more powerful

The biggest problem with travel reward cards is not earning points. The real challenge is redeeming them well.

Many users collect points but never use them properly. Some do not have travel plans. Some cannot find award seats. Some do not want to track multiple loyalty programs. Some simply want clean value without spending hours comparing transfer partners.

This update solves that problem beautifully. Axis Atlas users now have a practical fallback option. If travel redemptions are not working for you, your EDGE Miles are still useful at a fixed value of ₹1 per mile.

That makes Atlas more flexible than before. It still remains a strong travel card because of the 1:2 transfer ratio, but now it also gives users a simple redemption route when travel plans are uncertain.

This is exactly what makes the card more balanced now.

When should you use EDGE Miles for bill payment?

Using EDGE Miles for credit card bill payment makes sense when you do not have any upcoming travel plan, when award seats are not available, or when hotel redemption are not giving good value and you might need funds or emergency situation.

It can also make sense if you want a simple and guaranteed value instead of moving points into a loyalty program without a clear plan. Transferring points blindly is one of the easiest ways to reduce value. Once points move to a loyalty program, they are usually locked there. If you do not have a confirmed redemption in mind, the transfer may not help you immediately.

In that situation, redeeming EDGE Miles at ₹1 per mile towards your card bill can be a clean and practical choice for few people.

When should you avoid bill payment redemption?

You should avoid using EDGE Miles for bill payment if you already have a strong travel redemption in mind. You don't require funds to pay your credit card bills. There is no emergency situation.

If you are planning a vacation, first check airline and hotel partners. Look at the transfer ratio, award seat availability, hotel pricing, taxes, cash fares and redemption value. If the transfer partner route gives you better value than ₹1 per EDGE Mile, it makes more sense to transfer your points.

You can play the miles game here: https://app.book1a.com/transfers?source=1380

For example, 6,000 EDGE Miles can give you ₹6,000 bill value. But if the same 6,000 EDGE Miles become 12,000 airline miles and help you book a flight worth significantly more than ₹6,000, the transfer route is clearly better.

This is why the new bill payment option should not be treated as the default redemption. It should be treated as a safety net.

The Book1A view

For me, transfer partners still bring more value to the table when used properly. The 1:2 transfer ratio is the core strength of Axis Atlas, and that is where the card can outperform simple cashback products.

But I also like this update because it makes Atlas more practical for a wider set of users. Not everyone wants to search award seats. Not everyone has fixed travel dates. Not every hotel redemption gives good value. In those cases, having the option to use EDGE Miles at ₹1 per mile towards bill payment is genuinely useful.

The smart way to use Atlas now is simple: compare before redeeming.

Before burning EDGE Miles for bill payment, check transfer partners. Check airline miles. Check hotel points. Check award seats. Check the real cash price of the flight or hotel. Then compare that value against the fixed ₹1 per EDGE Mile bill payment option.

You can check transfer ratios and routes for Axis Atlas and other credit cards inside the TRANSFER section on the Book1A dashboard. We are building Book1A for credit card optimizers, travellers and people who want to make better decisions with their points instead of guessing.

By the way, this is exactly why we are building Book1A.

Most people have credit cards, reward points, vouchers, miles, hotel memberships and offers scattered across different apps, emails, screenshots and memory. The problem is not just earning points. The real problem is knowing what you own, where it can be used, when it expires, and how to extract the best value from it.

That is where Book1A starts.

Our free Onboarding plan gives you access to your own Book1A dashboard, where you can track your cards, points, miles, vouchers, expiry dates, transfer routes, hotel deals, Store1A offers and important rewards updates in one place. It is built for anyone who wants their points life to finally feel organised.

But if you want to go beyond tracking and actually build a strategy, Book1A also offers personalised credit card consultancy.

Because your points were never meant to sit idle. They were meant to take you somewhere.

We help you build a personalised roadmap for your cards, spends, points, miles and travel goals. From choosing the right card for the right expense to optimising reward points, milestone benefits, transfer partners, hotel stays and flight redemptions, we create a clear strategy around your lifestyle.

This is for people who want to enjoy the real power of credit card rewards without spending hours doing maths, comparing permutations, checking caps, reading fine print and second-guessing every redemption.

You focus on better vacations, better hotels, better flights and better savings.

We focus on the strategy.

A free dashboard to bring everything in one place.

A paid consultancy layer when you want a complete credit card and rewards roadmap.

And a smarter way to make your points work harder for you.

Final thoughts

Axis Atlas has become more flexible with this update.

Earlier, it was mainly a travel rewards card built around EDGE Miles and transfer partners. Now, it can also work like a cashback-style card when needed. That does not replace the transfer partner value, but it gives users a clean alternative.

If you have a strong travel plan, transfer partners can still deliver better value.

If you do not have a clear travel plan, bill payment gives you guaranteed value.

If you are unsure, compare both routes before burning your EDGE Miles.

That is the real power of Axis Atlas now. Your EDGE Miles can either become cash-style value against your bill or travel value through airline and hotel partners.

The smartest redemption is the one that fits your actual situation.

Featured card

Axis Horizon Credit Card

₹3,000 join · 5,000 EDGE Miles welcome · 40 lounge visits

Complimentary Runway Plan when your new card is activated

Apply now