I Spent ₹4,00,000 on AMEX Credit Cards and Got a 5-Day Sri Lanka Vacation Worth ₹1.7L for free. Almost 35% to 42% value on my spends.

How ₹4L of disciplined Amex spends became 1,12,578 Membership Rewards points — and a five-night Marriott stay in Sri Lanka worth up to ₹1.7L. The full maths.

In 2024 and 2025, I followed a simple but disciplined AMEX credit card strategy.

The result?

I spent around ₹4,01,250 across my AMEX cards, earned 1,12,578 Membership Rewards points, transferred them to Marriott Bonvoy, and redeemed 108,000 Marriott points for a 5-day stay at Weligama Bay Marriott Resort & Spa, Sri Lanka in November 2025.

The cash price of the same stay?

Depending on the dates, it was roughly ₹1,40,000 to ₹1,70,000.

That means my credit card points gave me a value back of around 30% to 42% on my total spends.

Sounds crazy, right?

Let me show you the full maths.

The Story: From Regular Spends to a Beach Vacation

This was my first-ever Marriott redemption, and honestly, it was a banger.

A luxury beach resort in Sri Lanka, ocean views, Marriott hospitality, and a stay that would have otherwise cost me well over a lakh in cash.

But the best part?

I did not earn these points by doing anything unrealistic.

I used a mix of:

- Welcome bonus points

- Monthly milestone bonuses

- AMEX Gyftr multiplier spends

- Referral points

- Platinum Travel milestone points

- Bought points

- Regular card spends

The strategy was simple: route planned spends through the right AMEX card at the right place.

Part 1: The Boost Month

In one strong month, I earned 42,778 AMEX MR points by spending around ₹97,450.

This came from three AMEX cards:

- AMEX Gold Charge Card

- AMEX Platinum Travel Card

- AMEX MRCC Card

Here is the complete breakdown.

1. AMEX Gold Charge Card

Points Earned

| Source | MR Points |

|---|---|

| Welcome bonus | 4,000 |

| Monthly bonus for 6 transactions | 1,000 |

| Regular spends + AMEX Multiplier | 2,093 |

| Total points earned | 7,093 |

Amount Spent

| Expense | Amount |

|---|---|

| Joining fee | ₹1,180 |

| Card spends | ₹21,250 |

| Total outflow | ₹22,430 |

So from the Gold Charge Card, I earned 7,093 MR points with an outflow of ₹22,430.

2. AMEX Platinum Travel Card

Points Earned

| Source | MR Points |

|---|---|

| Welcome bonus | 10,000 |

| Points bought | 10,000 |

| Referral bonus | 8,000 |

| Regular spends + AMEX Multiplier | 1,775 |

| Total points earned | 29,775 |

Amount Spent

| Expense | Amount |

|---|---|

| Joining fee | ₹4,130 |

| Buying points | ₹4,000 |

| Card spends | ₹42,920 |

| Total outflow | ₹51,050 |

The Platinum Travel Card gave me the biggest boost in this month: 29,775 MR points.

3. AMEX MRCC Card

Points Earned

| Source | MR Points |

|---|---|

| Welcome bonus | 4,000 |

| Monthly bonus for 4 transactions | 1,000 |

| Regular spends + AMEX Multiplier | 910 |

| Total points earned | 5,910 |

Amount Spent

| Expense | Amount |

|---|---|

| Joining fee | ₹1,180 |

| Regular spends + AMEX Multiplier | ₹22,790 |

| Total outflow | ₹23,970 |

The MRCC added another 5,910 MR points.

Boost Month Summary

| Card | MR Points Earned | Total Outflow |

|---|---|---|

| AMEX Gold Charge | 7,093 | ₹22,430 |

| AMEX Platinum Travel | 29,775 | ₹51,050 |

| AMEX MRCC | 5,910 | ₹23,970 |

| Total | 42,778 | ₹97,450 |

So in one month, I spent approximately ₹97,450 and earned 42,778 MR points.

That was the foundation of the entire redemption.

Part 2: The 6-Month AMEX Playbook

After the boost month, I followed a more structured AMEX strategy for the next 6-7 months.

The goal was simple:

Use each card where it gives the best return.

1. AMEX Gold Charge Card Strategy

For the AMEX Gold Charge Card, I used Gyftr 5X.

The normal earning rate is:

Base reward rate = 2 MR points per ₹100

Gyftr 5X reward rate = 10 MR points per ₹100

Monthly plan:

6 transactions × ₹1,000 = ₹6,000 monthly spend

Points earned:

₹6,000 × 10 MR / ₹100 = 600 MR points

Monthly bonus = 1,000 MR points

Total = 600 + 1,000

Total = 1,600 MR points per month

For 6 months:

₹6,000 × 6 = ₹36,000 spend

1,600 MR × 6 = 9,600 MR points

Gold Charge Summary

| Metric | Value |

|---|---|

| Monthly spend | ₹6,000 |

| Monthly MR points | 1,600 |

| 6-month spend | ₹36,000 |

| 6-month MR points | 9,600 |

2. AMEX MRCC Strategy

For the MRCC card, I used a mix of Gyftr 2X and monthly milestone bonuses.

The normal earning rate is:

Base reward rate = 2 MR points per ₹100

Gyftr 2X reward rate = 4 MR points per ₹100

Monthly plan:

First ₹6,000 spend:

4 transactions × ₹1,500 = ₹6,000

Additional spend:

₹14,000

Total monthly spend = ₹20,000

Points calculation:

On ₹6,000:

₹6,000 × 4 MR / ₹100 = 240 MR

Monthly bonus for 4 transactions = 1,000 MR

On additional ₹14,000:

₹14,000 × 4 MR / ₹100 = 560 MR

Monthly ₹20,000 milestone bonus = 1,000 MR

Total monthly points:

240 + 1,000 + 560 + 1,000 = 2,800 MR points

For 6 months:

₹20,000 × 6 = ₹1,20,000 spend

2,800 MR × 6 = 16,800 MR points

MRCC Summary

| Metric | Value |

|---|---|

| Monthly spend | ₹20,000 |

| Monthly MR points | 2,800 |

| 6-month spend | ₹1,20,000 |

| 6-month MR points | 16,800 |

3. AMEX Platinum Travel Strategy

For the AMEX Platinum Travel Card, I used Gyftr 3X and also worked towards the milestone.

The reward rate:

Base reward rate = 2 MR points per ₹100

Gyftr 3X reward rate = 6 MR points per ₹100

I spent approximately:

₹24,000 per month

Over the period, I hit around:

₹1.90 lakh milestone spend

Regular points earned:

₹1,40,000 approx eligible multiplier spend × 6 MR / ₹100

= 8,400 MR points

Milestone bonus:

15,000 MR points

Platinum Travel Summary

| Metric | Value |

|---|---|

| Approx monthly spend | ₹24,000 |

| Milestone spend hit | ~₹1,90,000 |

| Regular MR points | 8,400 |

| Milestone bonus | 15,000 |

| Total MR points | 23,400 |

Part 3: Total Points Earned

Now let’s combine everything.

Regular 6-Month Strategy

| Card / Source | MR Points |

|---|---|

| AMEX Gold Charge | 9,600 |

| AMEX MRCC | 16,800 |

| AMEX Platinum Travel regular points | 8,400 |

| Platinum Travel milestone bonus | 15,000 |

| Total from regular strategy | 49,800 |

Then I added my boost month and referrals.

| Source | MR Points |

|---|---|

| Regular 6-month strategy | 49,800 |

| Boost month points | 42,778 |

| Referral points | ~20,000 |

| Grand total | 1,12,578 MR points |

So the final total was:

34,800 regular points

+ 15,000 milestone points

+ 42,778 boost month points

+ 20,000 referral points

= 1,12,578 MR points

Part 4: Total Money Spent

Now let’s look at the actual outflow.

| Source | Amount |

|---|---|

| Regular 6-month strategy spends | ₹2,95,800 |

| Boost month outflow | ₹97,450 |

| Referral-related outflow | ₹8,000 |

| Total outflow | ₹4,01,250 |

So the total spend was:

₹2,95,800 + ₹97,450 + ₹8,000

= ₹4,01,250

Part 5: The Marriott Redemption

I transferred my AMEX MR points to Marriott Bonvoy and booked a stay at:

Weligama Bay Marriott Resort & Spa, Sri Lanka

Redemption cost:

108,000 Marriott points

Cash price of the same stay:

₹1,40,000 to ₹1,70,000

This was for a 5-day vacation in November 2025.

Part 6: Value Back Calculation

Now let’s calculate the value I received.

Total outflow:

₹4,01,250

Value of hotel stay:

₹1,40,000 to ₹1,70,000

Value back percentage:

Value back = Hotel cash price / Total outflow × 100

Lower-end value:

₹1,40,000 / ₹4,01,250 × 100

= 34.9%

Higher-end value:

₹1,70,000 / ₹4,01,250 × 100

= 42.4%

So my actual value back was approximately:

35% to 42%

If you consider only the rounded spend of ₹4,00,000, the maths becomes:

₹1,40,000 / ₹4,00,000 × 100 = 35%

₹1,70,000 / ₹4,00,000 × 100 = 42.5%

That is how I got nearly 35%-42% value back on my AMEX spends.

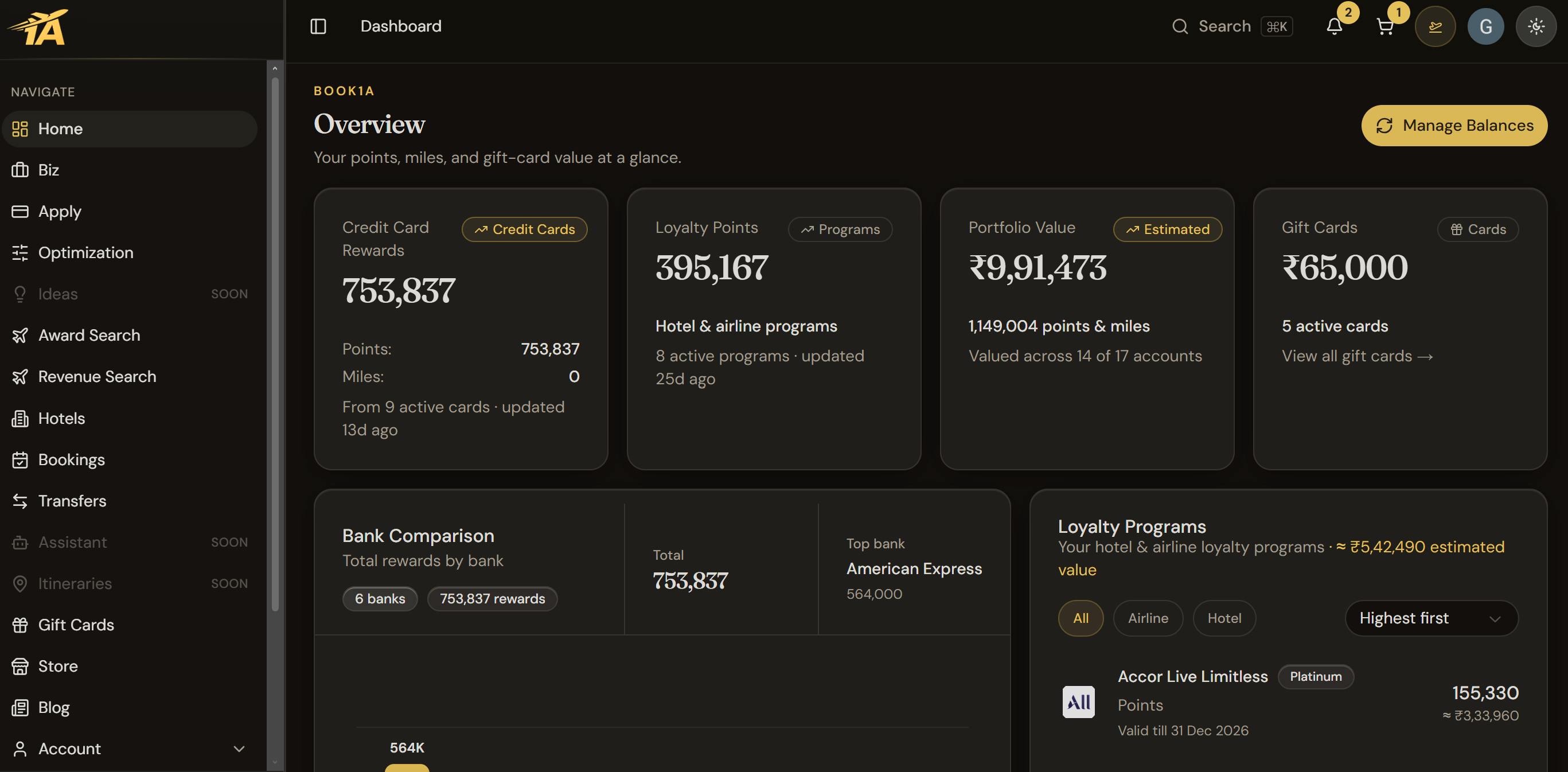

By the way, at Book1A, we also offer personalized credit card consultancy to help you take your rewards game to the next level.

Because your points were never meant to sit idle. They were meant to take you somewhere. ✈️

We help you unlock the true value of your reward points by creating a personalized blueprint and roadmap for your upcoming spends.

From choosing the right card for the right expense to optimizing reward points, milestone benefits, hotel stays, flight redemptions and transfer partners, we build the strategy for you.

This is for people who want to enjoy the power of reward points without spending hours doing maths, permutations and combinations. You leave the planning to us.

We help you optimize your cards, points and spends, so you can focus on enjoying better vacations, better hotels and better savings. With our consultancy, you also get access to your own unified dashboard, curated offers, hotel booking benefits, transfer partner tracking, reward optimization and other premium services.

A small consultancy fee.

A complete credit card and rewards strategy.

And a smarter way to make your points work for you.

By the way, this is exactly why we are building Book1A.

Most people have credit cards, reward points, vouchers, miles, hotel memberships and offers scattered across different apps, emails, screenshots and memory. The problem is not just earning points. The real problem is knowing what you own, where it can be used, when it expires, and how to extract the best value from it.

That is where Book1A starts.

Our free Onboarding plan gives you access to your own Book1A dashboard, where you can track your cards, points, miles, vouchers, expiry dates, transfer routes, hotel deals, Store1A offers and important rewards updates in one place. It is built for anyone who wants their points life to finally feel organised.

But if you want to go beyond tracking and actually build a strategy, Book1A also offers personalised credit card consultancy.

Because your points were never meant to sit idle. They were meant to take you somewhere.

We help you build a personalised roadmap for your cards, spends, points, miles and travel goals. From choosing the right card for the right expense to optimising reward points, milestone benefits, transfer partners, hotel stays and flight redemptions, we create a clear strategy around your lifestyle.

This is for people who want to enjoy the real power of credit card rewards without spending hours doing maths, comparing permutations, checking caps, reading fine print and second-guessing every redemption.

You focus on better vacations, better hotels, better flights and better savings.

We focus on the strategy.

A free dashboard to bring everything in one place.

A paid consultancy layer when you want a complete credit card and rewards roadmap.

And a smarter way to make your points work harder for you.

Final Summary

| Metric | Value |

|---|---|

| Total AMEX outflow | ₹4,01,250 |

| Total MR points earned | 1,12,578 |

| Marriott points used | 108,000 |

| Hotel booked | Weligama Bay Marriott Resort & Spa, Sri Lanka |

| Redemption date | November 2025 |

| Cash price of stay | ₹1,40,000-₹1,70,000 |

| Value back | ~35%-42% |

Final Thoughts

This was not a random points jackpot.

It was a planned AMEX strategy.

I used welcome bonuses, milestone bonuses, Gyftr multiplier spends, referral bonuses, and Marriott redemptions together. Individually, none of these looked life-changing. But when stacked properly, they turned regular spending into a luxury beach vacation.

The biggest lesson?

Credit card rewards are powerful only when you use them with planning.

Spend unnecessarily, and points become a trap.

Spend intentionally, and points can turn into experiences you would otherwise hesitate to pay cash for.

For me, that experience was a 5-day stay at Weligama Bay Marriott Resort & Spa in Sri Lanka.

Cash price: ₹1.4L-₹1.7L

Points used: 108,000 Marriott points

Total AMEX strategy spend: ₹4.01L

Value back: around 35%-42%

And yes, for a first Marriott redemption, this one was absolutely worth it.

Featured card

Amex Platinum Reserve Credit Card

₹10,000 join · 11,000 MR welcome · airport lounge access

Complimentary Runway Plan when your new card is activated

Apply now